Election Considerations: Is VP Kamala Harris's $25k homeownership grant proposal “crippling of an already weak economy"?

As featured in Inman News and Kiplinger Personal Finance.

With election day less than one month away, there has been much talk about a particular proposal by Vice President Kamala Harris, so let’s get into it:

“My administration will provide first-time homebuyers with $25,000 to help with the down payment on a new home.” – VP Kamala Harris

I have seen Instagram comments range from, excitement like, “This is major! This absolutely needs to be in place,” by Quiana Watson, Reality TV and Luxury Real Estate Broker.

And, "Omg I could maybe afford a house. That would change my life," by commenter Jill Anderson.

To concerned discourse via email that expresses that Harris’s grant (and other proposals) would be, “inflationary at best and would be crippling of an already weak economy at worst,” by Greg Blatt, past president of Dayton Realtors.

To borrow from Shakespeare, there has been “much ado” perhaps over nothing.

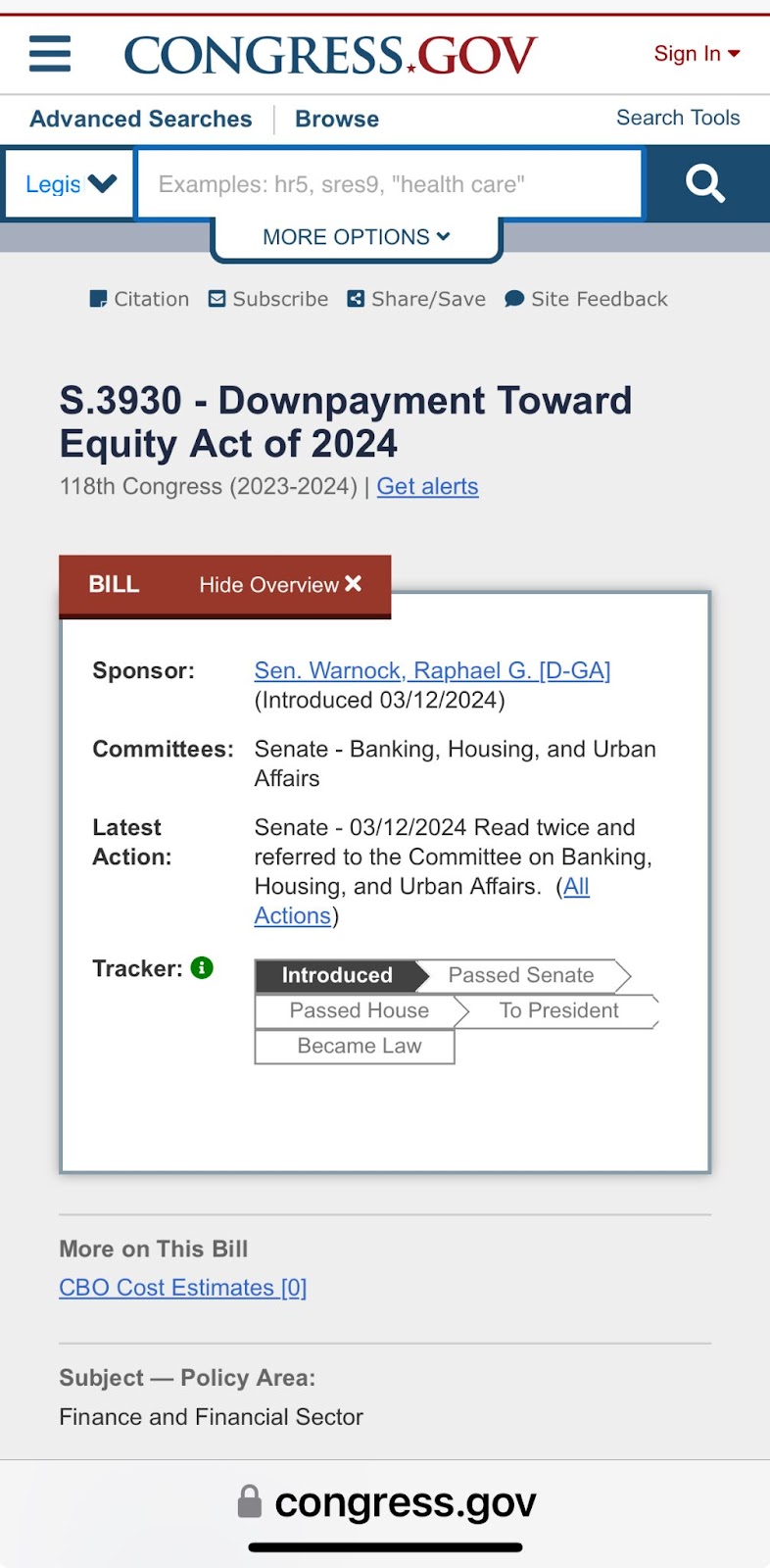

The Downpayment Toward Equity Act of 2021 (2022, 2023 and 2024)

Quiet as it is kept, Harris's plan to offer $25,000 for first-generation, first-time homebuyers is already on the books. The Downpayment Toward Equity Act — also known as the $25,000 First-Time Home Buyer Grant or the Downpayment Toward Equity Act — would give eligible first-generation first-time homebuyers in the U.S. up to $25,000 to put toward the purchase of a home. The funds could be used for costs such as the downpayment, mortgage closing costs or a lower mortgage rate. The Act was originally introduced in 2021.

It is still in the current administration's budget proposal, however, it has not been enacted yet.

But what if Harris's administration, if elected, miraculously compels the stars of the Senate and House to align?

Assistance Funds Often Get the Cold Shoulder

As an affordable, fair housing educator who has helped many a first-time homebuyer use downpayment grant programs (there are over 2,415 which help to increase homeownership), I believe the next and better question (if the act or some variation is finally passed) is not how it will impact the economy but rather if sellers will work with homebuyers that use such downpayment assistance.

The adoption of the program and participation by home sellers will determine if this becomes even a blip on the economy’s radar.

Historically, the answer is some sellers will work with downpayment assistance programs but a lot more will not (many of us know this anecdotally). This is especially true if the downpayment program is structured like existing programs, which may require extra time for homebuying classes, inspections and additional financial verifications, whether those time and administrative obstacles are exaggerated or true horror stories.

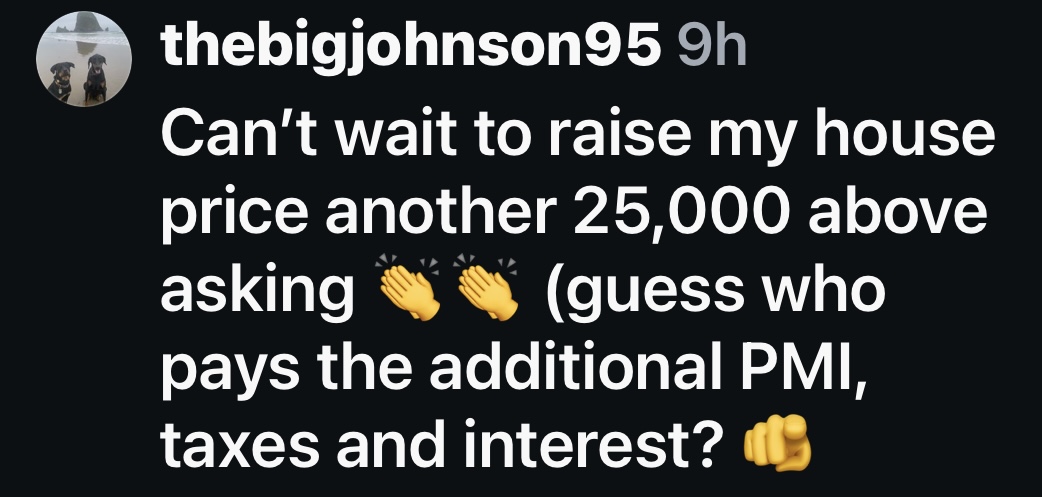

A speedy commenter on Instagram underscores that some home sellers resist such programs:

“Can’t wait to raise my house price another 25,000 above asking (guess who pays the additional PMI, taxes and interest?)”

Again, this highlights that the first question is not how this impacts the economy but whether home sellers will participate despite historical trends and negative sentiments.

To add a few more hurdles to this herculean journey, “source of income” (which these assistance funds would fall under) is not a federally protected class. That means only the handful of locations that have “source of income” protection laws with general provisions (that cover downpayment assistance) could possibly penalize home sellers for rejecting a homebuyer solely on using downpayment assistance funds.

Again, historically, the disregard of “source of income” protections happens more than it should. Case in point, the housing choice voucher program (a.k.a. "Section 8") has the most legal protections of the “source of income” designation currently. Notwithstanding existing laws, a recent lawsuit was filed against 203 California landlords and their representatives — including major real estate brokerages.

Unsurprisingly, some first-time homebuyer grant programs end a fiscal year still funded because of how much harder finding a suitable home is for prospective homebuyers using downpayment assistance.

Thus, before forecasting the impact on the economy, we really need to hear (and help strategize since we have boots on the ground) how a federal downpayment grant program will be administered in a more home-seller-friendly way to circumvent the hurdles that other downpayment grant programs (as well as other "source of income" programs like "Section 8") have documented in detail. For example, what incentives can be provided to encourage home seller participation in downpayment assistance programs in general?

Home-Seller-Friendly Downpayment Programs Are a Pre-Req.

As a fair housing D.E.C.O.D.E.R., I teach in continuing education classes that it is important for us to emphasize more “carrot cake” activities (positively incentivizing fair housing proactiveness) and not simply the “stick” approach (which exclusively seem to focus on punitive enforcement). Surely, there is a place for correction and restitution when laws are broken, but there is more buy-in when we emphasize the “carrot cake” motivation theory. (Sidebar: I know this theory is based on horses and they like plain carrots but as humans, give me carrot cake please, ha!)

An interesting conversation started in my Instagram comments surrounding what if home sellers (because they likely are going to need to buy a home too) who closed with home buyers using downpayment funds could also have access to these downpayment programs despite not being first-generation or first-time buyers? Perhaps it is not the full amount that the buyer who needed the assistance got, but history has shown us that there needs to be some sort of incentive.

Otherwise, the economic impact will likely be inconsequential – it becomes more a token of goodwill rather than a substantive and widely adopted program.

Dr. Lee Davenport is a real estate coach/educator and author (including Be a Fair Housing D.E.C.O.D.E.R. and How to Profit with Your Personality). Dr. Lee trains real estate agents around the globe on how to work smarter with their unique personalities and how to “advocate, not alienate,” so everyone has access and opportunity in real estate.

Have you ever needed the “Cliff Notes” version of fair housing? Well, move over Spark Notes!

The Starting Point: How to Be a Fair Housing DECODER Guide https://books.bookfunnel.com/learnwithdrlee

It is available to download for a limited time at no fee. Score!

This condensed workbook (based on the nationally acclaimed workshop) offers Dr. Lee's novel concept of being a Fair Housing DECODER© who skillfully and proactively advocates --not alienates-- for equitable access and opportunity in real estate for EVERYONE.

“Interesting approach on the topic of fair housing that I have not seen offered to Realtors.” --Maria, Broker/Owner, REALTOR®

“I have the Realtor GRI designation and they should make this part of that designation. This is THAT good. THANKS, Dr. Lee!” --Michael, Broker/Owner, REALTOR®

Hurry, download (and share with others) today while complimentary supplies last!